California’s Billionaire Tax Will Reduce State Revenues

Results of a New Hoover Institution Analysis

Back in January, I argued that California’s proposed one-time billionaire wealth tax was fiscally and economically unsound. The basic argument was straightforward: When a tax applies to a narrow, highly mobile base and hinges on residency at a single point in time, it does not take a mass exodus to undermine the policy. It takes only a few departures from the taxpayers who already contribute a disproportionate share of state revenues.

A new Hoover Institution report by Joshua Rauh, Benjamin Jaros, Gregory Kearney, John Doran and Matheus Cosso suggests the policy may be even less viable than I initially described. The authors find that, accounting not only for reduced wealth tax collections, but also for the future income taxes California would lose if billionaires leave, the wealth tax likely produces a negative net fiscal return. In other words, this is not merely a tax that raises less than advertised, but one that will actually leave the state coffers worse off.

Loss of Tax Base

The California Billionaire Tax Act would impose a one-time 5% tax on the worldwide net worth of individuals worth more than $1 billion if they were California residents or part-year residents on January 1, 2026. Supporters have advertised the measure as a way to raise roughly $100 billion. But Rauh and his coauthors argue that this estimate rests on a deeply unrealistic view of both the tax base and taxpayer behavior.

They begin by estimating how large the tax base is for this type of tax. Using the 2025 Forbes billionaire list, publicly available information on residency, and property holdings, they conclude that the proponents’ baseline estimate was overstated from the outset. Some individuals included in the original tally were no longer California residents, and the proponents also appear to have ignored statutory exclusions for directly held residential real estate. Even before considering tax avoidance, the authors estimate that the realistic no-behavioral-response revenue figure is about $94 billion rather than $100 billion.

The more important issue is that the policy has already induced behavioral responses before enactment. According to the report, six publicly confirmed departures before the January 1 snapshot date removed more than $536 billion from California’s tax base—nearly 30% of the total. With those departures alone, projected revenue falls from roughly $94 billion to about $67.5 billion.

That finding by itself should destroy the comforting fiction that “one-time” means economically harmless. A one-time levy pegged to a fixed residency date can be especially distortionary because it creates a clear incentive for taxpayers to leave before the trigger date arrives. California’s proposal did not merely create a future obligation; it created an immediate scramble to establish outside options.

The authors then argue that the publicly confirmed departures likely understate the true migration response because many high-net-worth individuals have strong reasons not to announce their plans. Drawing on wealth tax literature and evidence from migration responses abroad, the authors estimate that actual wealth tax collections will likely be around $40 billion, with a range of roughly $35 billion to $46 billion. That is less than half of the amount promised by the measure’s proponents.

Loss of Future Income Tax Revenue

If the analysis ended there, the initiative would already look fiscally dubious. But the most important contribution of the paper is that it does not stop with the wealth tax itself. The authors ask the question many advocates prefer to avoid: What is California giving up in exchange for this one-time payment?

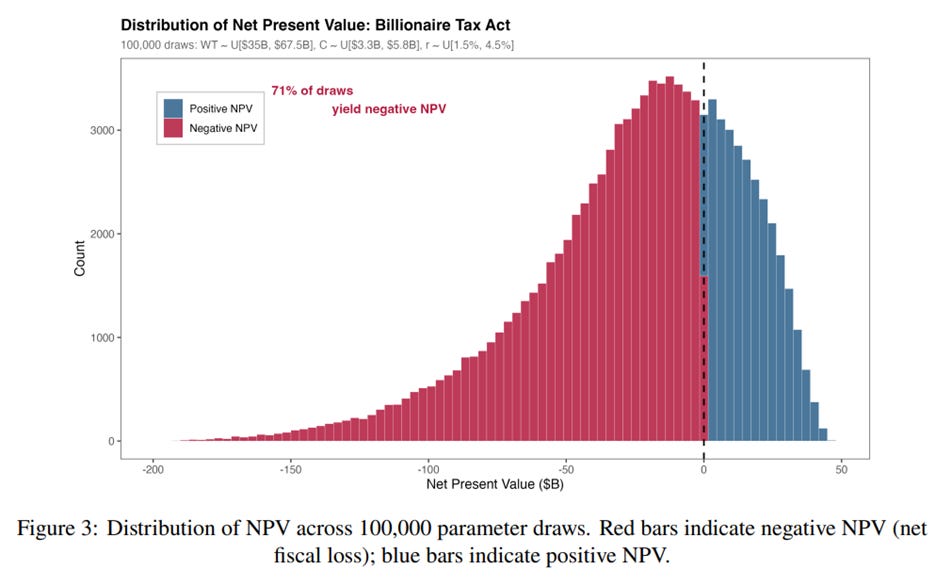

The answer matters because California’s tax system is extraordinarily dependent on a relatively small number of high-income taxpayers. Rauh and his coauthors estimate that the state’s 212 billionaires generate between $3.3 billion and $5.8 billion annually in state income tax revenue. If a large portion of them leave in response to the wealth tax, those future tax payments disappear. Since the wealth tax generates a one-time burst of revenue but the loss of income taxes extends into the future, the proper way to evaluate the proposal is through net present value.

Across a broad range of assumptions about revenue, discount rates and income tax losses, the authors estimate an average net present value for this wealth tax of negative $24.7 billion. In their simulations, 71% of plausible outcomes produce a negative fiscal result (see figure from the report below). The state gets an upfront payment, but the present value of forgone future income tax collections is often larger.

This is an important shift in how the debate should be framed. Too much of the public discussion has focused on whether the measure will raise $100 billion or “only” $40 billion. But that is the wrong benchmark. The relevant question is not simply how much comes in at time zero, but whether the state comes out ahead after accounting for the future revenue stream it sacrifices by driving away a portion of its existing tax base.

Other Economic Losses

Even this framing of the question may understate the policy’s damage. As the authors note, the fiscal estimates do not fully capture broader economic losses from reduced investment, business formation, employment and entrepreneurial activity. Billionaires who leave California do not just stop paying California income taxes. They may also stop founding companies there, funding startups there or employing large numbers of high-income workers there.

The report also casts doubt on the claim that this is truly a “one-time” tax in any meaningful sense. Formally, the initiative is a constitutional amendment that would remove California’s existing cap on taxes on intangible personal property. Once that guardrail is gone, future wealth taxes become easier to enact. That means affected taxpayers are not irrational if they treat this proposal as a precedent rather than a one-off emergency measure. In a state with a history of extending “temporary” tax hikes, skepticism is entirely warranted.

In January, I argued that California’s billionaire tax would likely fail because it relied on the mistaken assumption that a small number of highly mobile taxpayers would absorb major new uncertainty without changing their behavior. The Hoover report strengthens that case considerably. It suggests not only that the tax would raise far less than advertised, but that after accounting for lost income tax revenue, it would likely leave California with a negative return.

The real lesson here is that wealth taxes do not become sound policy just because they are targeted at unpopular people or sold as emergency measures. Economic principles still apply. Tax a narrow, mobile, difficult-to-measure base, and you should expect avoidance, migration, administrative conflict and disappointing (or in this case negative) revenues. California’s billionaire tax is shaping up to be a textbook example.

“According to the report, six publicly confirmed departures before the January 1 snapshot date removed more than $536 billion from California’s tax base”

Who are the 6 confirmed departures? I presume to be that large it’s gotta include one or both of the Google guys.