Debt Is Not a Free Lunch

New Policy Brief on channels, thresholds, and the role of monetary policy absorption in the Debt-Growth relationship

The empirical literature on public debt and economic growth is now vast, and a central conclusion has emerged: high and rising debt is associated with slower growth. Nevertheless, many economists still treat the relationship as unsettled or deny that it exists altogether.

In a Mercatus review of 80 empirical studies published between 2010 and 2025, I found that high and rising public debt is consistently associated with slower economic growth. The central estimate across studies suggests that each additional percentage point of debt-to-GDP reduces economic growth by about 3.3 basis points.

So, the real puzzle is not whether debt matters. Most of the evidence says it does.

The puzzle is why a smaller group of studies, especially those finding no clear relationship between debt and growth, receives such disproportionate attention from those who want to understate the costs of borrowing. These studies are politically convenient. If debt has no measurable effect on growth, then there is no need to confront tradeoffs. Expansive spending plans can be presented as painless. New programs can be financed through borrowing rather than taxes. The bill can be pushed into the future, while the benefits are enjoyed today.

But the “no effect” conclusion usually rests on a misleading empirical setup.

In my latest policy brief, I use quarterly U.S. data from 1975 through 2025 to show why simple regressions can fail to detect the growth costs of debt. The problem is not that debt has no effect. The problem is that conventional total-effect regressions often combine several channels that move in opposite directions.

Debt-financed spending can raise measured GDP in the short run. Government outlays enter aggregate demand directly, so borrowing to spend more can temporarily boost output. But over time, public debt can also suppress private capital formation. When government borrowing absorbs resources that would otherwise flow into productive private investment, the economy accumulates less capital. Less capital means lower productivity, weaker wage growth, and slower long-run output growth.

Put both effects into the same regression, and they can cancel each other out. The result is a coefficient near zero, not because debt is harmless, but because the regression is measuring the net of a short-run demand boost and a long-run supply-side cost.

That is the key distinction. The right question is not merely whether debt and GDP growth are correlated in the aggregate. The right question is whether debt damages growth through identifiable economic channels.

And the answer is yes.

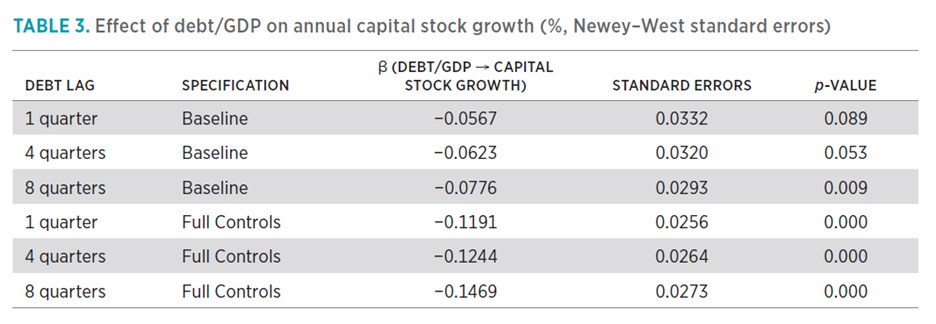

The first channel is capital accumulation. In the brief, I examine the relationship between federal debt held by the public as a share of GDP and the growth rate of the private nonresidential capital stock. This is a better measure than quarterly investment flows, which are noisy and volatile. Capital goods are durable. Their contribution to output unfolds over years. A factory, machine, or logistics network does not raise productivity for only one quarter. It adds to the economy’s productive capacity over time.

Using the capital stock measure, I find that a one percentage point increase in debt-to-GDP reduces annual private capital stock growth by roughly 0.12 to 0.15 percentage points, depending on the lag specification. This relationship remains statistically strong after controlling for inflation, unemployment, real yields, monetary policy, foreign demand for Treasurys, and other macroeconomic conditions.

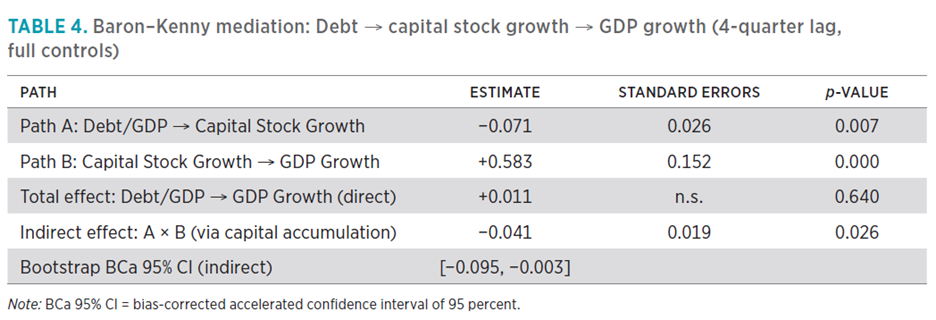

The second link is that capital stock growth predicts GDP growth. This is exactly what economic theory would lead us to expect. Economies grow richer when workers have more and better capital to work with. Investment flows bounce around from quarter to quarter, but the accumulated capital stock is what drives productive capacity.

Combining these two links gives the full channel: higher debt suppresses capital accumulation, and weaker capital accumulation suppresses growth. The mediation analysis in the brief confirms this indirect effect. The estimated negative effect is about -0.04 percentage points of GDP growth for every one percentage point increase in debt-to-GDP, with bootstrap confidence intervals entirely below zero.

That effect may sound modest, but growth effects compound. A small annual drag becomes a large loss over decades. And unlike a temporary stimulus effect which fades in time, a smaller capital stock represents a persistent reduction in the economy’s productive base.

The second major channel concerns interest rates.

The conventional crowding-out story is straightforward: higher government borrowing competes with private borrowers, pushes up yields, raises the cost of capital, and reduces investment. Critics of this view point to the post-2008 period and say: debt soared, yet interest rates stayed low. Therefore, they argue that the old fiscal constraints no longer apply.

But that argument ignores the Federal Reserve.

My brief finds that the Fed’s balance sheet suppressed the interest-rate transmission mechanism during the very period when debt was rising fastest. When the Fed holds less than about 14 percent of outstanding Treasurys, higher debt raises real yields in the conventional way. Once the Fed’s holdings exceed that threshold, the debt-yield relationship disappears and can even invert. During the post-2008 and post-2020 quantitative easing episodes, the Fed crossed that threshold.

In other words, the interest-rate channel did not vanish because debt stopped mattering. It was muted because the Fed was absorbing Treasury supply.

This distinction matters enormously. Low Treasury yields during the QE era do not prove that borrowing was costless. They show that the central bank was intervening in the market for government debt. But the Fed cannot conjure real resources into existence. Suppressing yields does not eliminate scarcity. It does not erase opportunity costs. And it does not guarantee that private capital formation remains unharmed.

Crowding out can occur through balance sheet allocation, credit channels, risk premia, and expectations of future taxation. Even when interest rates are low, financial institutions still decide whether to hold government securities or extend private credit. Firms still decide whether future tax burdens make long-term investment less attractive. Resources still have to be allocated between politically directed spending and market-tested capital formation.

That is why the absence of visible rate crowding out is not the same thing as the absence of crowding out.

The broader lesson is simple: debt is not free merely because some regressions fail to find a statistically significant total effect. The literature finds that high debt slows growth, and my latest brief helps explain the mechanism. Debt harms long-run growth by suppressing private capital accumulation. That damage is easy to miss when short-run demand effects and Fed balance sheet expansion are masking the underlying channel.

This is especially relevant now. Federal debt held by the public is about 100 percent of GDP, well above the threshold range identified in much of the empirical literature. If the Fed ends its balance sheet expansion and its Treasury share moves back toward pre-QE levels, the conventional interest-rate channel may reassert itself. That would add to the rate crowding out on top of the capital accumulation channel already visible in the data.

The fiscal debate should therefore move beyond the comforting claim that “we borrowed more and nothing bad happened.” Something did happen. The damage was simply slower, less visible, and partly obscured by monetary policy.

Debt-financed spending can make today’s GDP numbers look better. But the bill arrives through a smaller capital stock, weaker productivity growth, and lower future living standards.

Debt does matter. And pretending otherwise is granting permission to politicians to spend now and leave the costs to everyone else later.

Great article! Highly recommend it.