Ice Cream Cartels and MMT's Japanese Illusion

This is the first post in a guest series by a PGPF Summer Intern Dakota Stacy

Ice Cream Cartels and MMT’s Japanese Illusion

MMT economists often point to Japan’s debt as evidence that a country can avoid a fiscal crisis despite carrying a high debt burden, provided that the debt is properly managed. However, Japan has not escaped the consequences of its debt: it obscures the crisis through exports, hides it behind illiquid assets, shifts fiscal risk into foreign-exchange markets, and, of all things, incentivizes the formation of an ice cream cartel that fixes prices.

Is the debt questionable?

Particular economists when asked about Japan’s debt may give answers within a Modern Monetary Theory (MMT) framework, proposing that Japan cannot default as they print their own currency. In other words, the Bank of Japan (BOJ) is the biggest buyer of Japanese government issued bonds and becomes both the debtor and debt collector. The logical implication is that the best thing Japan could do would be to increase their borrowing and encourage consumption so long as inflation remains low.

Japan certainly does one of those things in plenty, borrowing, but has both a demographic that ranks among one of the highest saving populations in the world and within the last 10 years has doubled the VAT rate from 5% to 10%. Struggling with that lack of stimulus, Japan has tried to artificially trigger activity in three different phases from 1991-2024, but each time was woefully executed.

What then followed was Prime Minister Takaichi’s election in 2025 where she has continued to spend in grandiose ways unseen since Imperial Japan in 1945. Looking to the Cabinet Office figures, it puts gross liabilities at a staggering 270% over GDP.

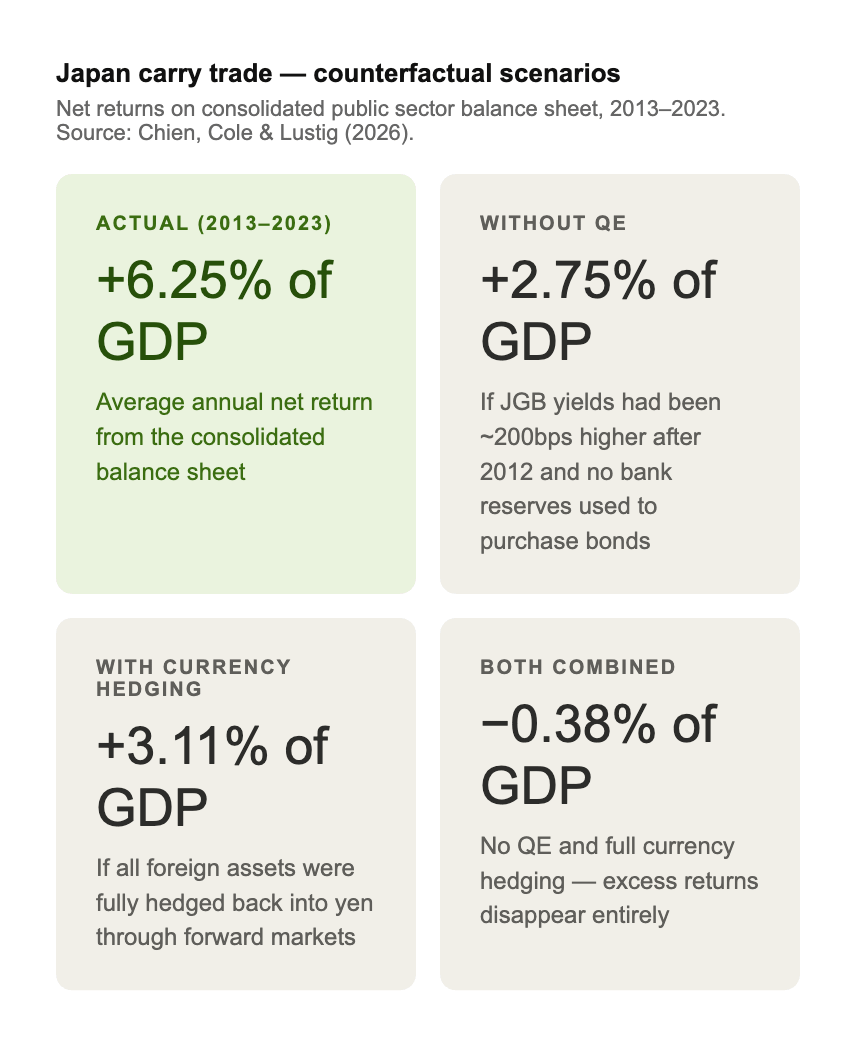

Many will say this isn’t as it seems though, because Japan owns considerable assets totaling 193% of GDP. An argument according to an article by Yili Chien, Wenxin Du, and Hanno Lustig, follows that Japan’s net debt is but a modest 77% of GDP in 2024. Of that figure, 88% is domestic, and of the domestic portion, 56% is held in the public sector. They argue that this gives Japan a highly leveraged Sovereign Wealth Fund (SWF) financed from cheap domestic borrowing, and such shields itself from foreign creditors. But, because most of the assets are borrowed money, the structure is fundamentally sensitive to changes in interest rates.

Interest Rates Are Up

The BoJ has held its rate near 0% for decades, but since 2024 has been steadily increasing it and amid turmoil surrounding the unpredictable Iran war, the BoJ chief has recently raised this rate to 1% in June. Consequently, the SWF’s balance sheet will face costs in the form of devalued assets, a significant part of the debt’s neutralizer. Moreover, because higher interest rates paradoxically weaken the yen due to the carry trade unwinding, Japanese consumers have to pay more for goods — and the government does too.

The Yen carry trade’s precariousness

Looking to Hanno Lustig, he wrote on Two Cents that “the result is a classic carry trade, just executed by a sovereign. Borrow at the short end of the curve at rates the BoJ controls. Invest at the long end — and in global equity markets, adding a currency carry trade, funded in yen. Pocket the spread” This was visualized via the graph below:

In an ideal world, the carry trade works – but things are never ideal. As Japanese 10-year bond yields continue to rise, so too does government funding costs.

And the yields are rising.

Trading Economics

Higher yields translate to higher interest rates, which means that a large share of Japan’s assets — Foreign based (primarily U.S.) — will become less valuable. This matters because whenever Japan’s government intervenes in supporting a weakening yen, they have to sell assets to then buy back yen with a stronger currency. But, because the assets they are selling are worth less than if the yields had not risen, a risk for realizing losses emerges. In essence, Japan’s foreign exchange defense grows weaker as the assets they might sell lose value.

The Pushback

MMT enthusiasts from Stephanie Kelton to Warren Mosler recently dismissed Japan’s debt by penning, “Japan is not trapped by its debt; it is choosing an interest-rate policy that weakens the yen and adds income”.

This idea of a weak yen being advantageous was then popularized by Joeri Schasfoort’s video on “Money and Macro” posted a few weeks ago, amassing over 250k views. Yet, in his conclusion he looks to Japan’s aging population and argues that while things currently are bearable, as Japan grows older and begins to spend more, inflation will inevitably rise. But, importantly, he hints that things are fine now.

Both the MMT crowd and Schasfoort look to a weak yen as beneficial for gains in exports and use it to sidestep what one might call a debt crisis. The logic is simple: Japan chooses this policy, generates more revenue through foreign demand for cheaper domestic goods, and has the agency to sell their assets if need be.

Debunking The Claims

1. Japan does not choose this policy. Rates were cut to zero because deflation was problematic, resulting in a weak yen as byproduct. It was not to design an elegant export strategy. Additionally, as those very rates begin to suddenly rise, so too does the yen weaken from a depreciation of foreign assets.

2. Relying on exports creates imbalances in other means, notably imports and domestic commerce. This creates costs for households as Japan imports most of its electricity and food. In an effort to mitigate the loss, the government has to take out even more debt on subsidies for utilities via taxes. This is a consequence happening now, which pushes back against Schasfoort’s idea that things are fine so long as inflation stays low. Moreover, Japanese ministers could learn from reading the research of Alberto Alesina on fiscal consolidation. Spending cuts, not tax increases, are most successful at reducing public debt over time. Additionally to that point, Jack Salmon recently published a paper writing:

“a one-percentage-point spending-based consolidation increases the probability of success by 11.1 percentage points, while a tax-based consolidation of equal magnitude reduces the probability by 9.5 percentage points.”

3. Higher yields means higher costs of borrowing, and an even larger interest payment on fiscal debt. Japan spends 40% of its tax revenue on debt interest, up 7% alone from rising interests rates in the past year. As Jack Salmon observed,

In its FY2025 budget, Japan spent roughly 33 cents of every tax dollar just servicing its debt. That was before yields on 10-year bonds roughly doubled to more recent levels […] In upcoming budgets, that figure is likely to creep toward 40 cents on the dollar. This is a remarkable constraint on fiscal policy for a country that supposedly “proved” debt doesn’t matter.

4. Japan does not have agency. I.e., it cannot up and sell much of anything. Most assets are tied to pensions which aren’t able to be sold en masse and are time constrained. I.e., the assets are structurally illiquid. Lastly, in all of this, there is an assumption that enough buyers exist for the 193% GDP valuation and will pay that current valuation before market absorption capacity lowers prices.

5. MMT may work in certain respects, but it doesn’t come without costs. Borrowing from Robin J Brooks to push back against the MMT argument, he wrote,

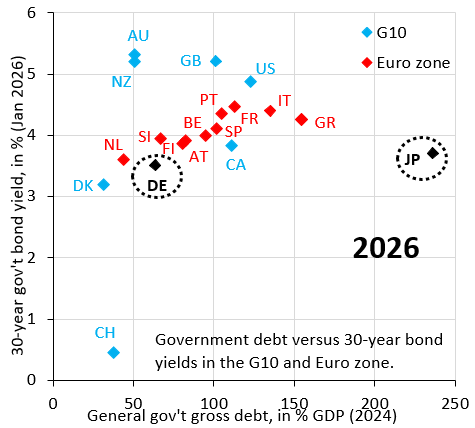

Japan’s 30-year yield is basically the same as Germany, which has much lower public debt. That’s a sign that fiscal risk premia in the bond market are being artificially suppressed via ongoing Bank of Japan bond purchases. However, these yield caps don’t cause the fiscal risk premium to disappear. It just manifests in foreign exchange markets, dragging down the Yen.

In other words, Japan’s fiscal risk premia should be significantly higher. But, because the BoJ distorts price signals from consistently buying JGBs and flooding the market overtime artificially lowering interest rates, investors instead sell Yen which weakens the value. In essence, Japan does not choose to weaken their currency; rather it is a consequence of nervous investors who recognize the problems of Japan’s debt.

Ice Cream Cartels & Inflation

To round things off with point 6, Pete Earle at The Freeman recently wrote:

For years, yen weakness failed to translate cleanly into domestic inflation because firms absorbed cost increases internally rather than fully passing them on to consumers. That pass-through has increased more recently, but even that change has occurred gradually and reluctantly

Pete’s focus was on how monetary and fiscal policy can shape a country’s norms and behaviors, and this quote maps perfectly onto an unexpected topic in Japan: Ice cream cartels.

Japan’s Fair Trade Commission (JFTC) recently raided six major ice cream manufacturers on suspicions of price fixing from 2022-2025. Instead of internally absorbing costs like they had done for decades, ice cream manufacturers allegedly took advantage of sudden inflation: collectively raising prices and blaming the increase on inflation. This is another unintended consequence of Japan’s debt: prices have been deflated so long through the BoJ’s suppression of rates that sudden inflation incentivized price coordination as opposed to market competition.

Debt Debunked: The Part I Conclusion

There are three ideas I want to leave you with today when considering Japan’s debt:

(1) High debt can’t come without tangible consequences

(2) Excessive utility subsidies, a weakening yen, inefficient tax expenditures, and for the love of all things, ice cream cartels, are current consequence of Japan’s debt

(3) Nothing is free, especially debt

Thank you for your time. I hope you may agree with the importance of this issue and that Japan does not coast in a calm sea of fiscal ingenuity. If you disagree though, please feel free to comment and I will promptly reply.