Obamacare’s Fraud Problem Is an Incentives Problem

A new paper from the Paragon Health Institute, The Persistent Obamacare Enrollment Fraud, documents a remarkable fact about the Affordable Care Act exchanges: even after the expiration of the COVID-era subsidy expansion, improper enrollment remains enormous.

Paragon estimates that roughly 6.2 million exchange sign-ups in 2026 were improper, representing about 27 percent of all ACA exchange sign-ups. The associated taxpayer cost could be as high as $25 billion this year. This is a predictable consequence of a program designed around excessive subsidies, weak verification, and third-party actors who are rewarded for maximizing enrollment rather than ensuring eligibility.

The core problem is simple. When government makes something “free” at the point of purchase, it does not eliminate cost. It changes who pays, who decides, and who has an incentive to police abuse. In the ACA exchanges, generous subsidies flow directly to insurers on behalf of enrollees. Many plans require little or no premium from the consumer. Brokers and enrollment intermediaries can receive commissions for placing people into plans. And if the applicant’s reported income qualifies them for the maximum subsidy, the transaction can be completed with minimal resistance.

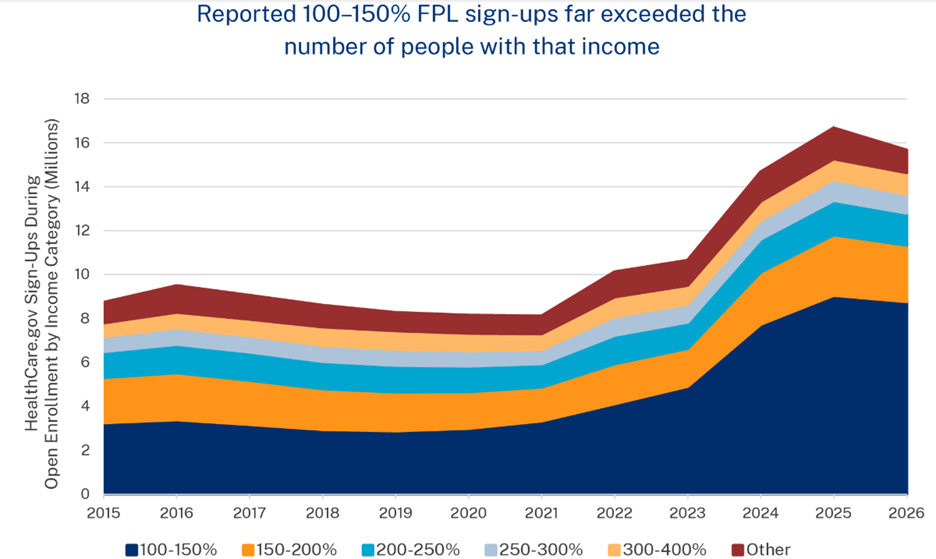

Paragon’s methodology focuses on the 100 to 150 percent of the federal poverty level income category, where ACA subsidies are most generous. The authors compare the number of people enrolled in that category with Census-based estimates of the plausibly eligible population. In many states, enrollment substantially exceeds the number of people who could reasonably be eligible. The excess is treated as improper enrollment.

That approach is not perfect, and Paragon is right to describe its estimates as estimates. But the scale of the mismatch is too large to wave away. In Florida, the paper estimates that improper enrollment is especially severe. Texas, Georgia, South Carolina, and North Carolina also account for a large share of the national problem. The pattern is not random. It is concentrated in states using HealthCare.gov, particularly non-expansion states where low-income individuals have a strong incentive to report income above the poverty line in order to qualify for exchange subsidies.

This is what economists mean when we talk about incentives. Policy does not merely transfer money; it creates margins of behavior.

The ACA created a cliff. People below 100 percent of the poverty line in non-expansion states generally do not qualify for exchange subsidies. People just above that threshold can qualify for large subsidies. Once policymakers draw that line, they should not be surprised when reported income clusters on the favorable side of it. Nor should they be surprised when brokers, insurers, and enrollment platforms discover that the most profitable customer is one whose premium is paid by Washington.

The problem is compounded by zero-premium plans. A plan with no monthly payment is much easier to sell, much easier to retain, and much easier to manipulate. If someone is enrolled without fully understanding what happened, there may be no monthly bill to alert them. If a broker switches a consumer into another plan, the consumer may not notice if the premium remains zero. If an enrollee never uses the plan, federal subsidy dollars can still flow.

Paragon points to evidence of “phantom enrollment,” including large numbers of exchange enrollees with no medical claims. Again, no single statistic proves fraud in every case. Some people are healthy, while some people enroll and simply do not need care. But when millions of people are enrolled in heavily subsidized coverage, many pay nothing, many have no claims, and enrollment exceeds plausible eligibility counts, the burden of proof should shift to those defending the status quo.

This is a recurring theme in modern progressive governance. A program is created to solve a real problem. Subsidies are expanded to make the program appear more generous. Administrative safeguards are relaxed to maximize take-up. Then, when predictable abuse follows, critics are told that concern over fraud is merely hostility to the poor.

But program integrity is not hostility to the poor. It is respect for taxpayers, for genuine beneficiaries, and for the rule of law.

Every dollar spent on improper enrollment is a dollar not available for deficit reduction, lower taxes, or better-targeted assistance. Worse, fraud and phantom enrollment corrupt the information policymakers use to evaluate the program. If enrollment numbers are inflated by people who are ineligible, unaware, duplicated, or not actually using coverage, then the headline enrollment statistics become propaganda rather than evidence.

The lesson here is that open-ended federal subsidies, routed through private intermediaries and enforced by weak verification, will predictably invite abuse. Washington tried to engineer affordability through third-party payment and bureaucratic formulas. The result was not discipline, transparency, or consumer control. It was a system in which insurers collect subsidies, brokers chase commissions, and taxpayers are left holding the bag.

Paragon recommends stronger eligibility verification, tighter identity authentication, stricter oversight of enrollment intermediaries, limits on automatic reenrollment, and reforms to zero-premium plan structures. Those are all sensible steps, but the deeper reform is to stop pretending that subsidized enrollment is the same thing as real coverage, and that federal spending is the same thing as health care.

Obamacare’s fraud problem is not an accident. It is the result of policy design. When government subsidizes something too generously, verifies eligibility too weakly, and measures success by how many people are signed up, it should expect exactly what Paragon finds: millions of questionable enrollments and billions of taxpayer dollars at risk.

Well said; for sure incentives matter across all aspects of life. As to this program, once again many fail to see the costs of good intentions.