Spending Cuts or Tax Increases: 38 Years of Data on Fixing the Debt

Every debate about fiscal consolidation eventually runs into the same fork: tax increases or spending cuts?

My new research paper brings fresh evidence to that question using narrative fiscal consolidation data for 17 advanced economies from 1978 to 2016. The main result is straightforward: Spending-based consolidations are associated with better growth outcomes and better debt-reduction outcomes than tax-based consolidations. And I find no evidence that this composition effect depends on whether a country starts with low, moderate, or high levels of debt.

Prior literature

Much of the fiscal consolidation literature finds that spending-based adjustments tend to be more successful than tax-based adjustments. The late Alberto Alesina spent more than two decades exploring this question, arguing that the composition of fiscal adjustment matters for both economic performance and debt reduction.

Veronique de Rugy and I published a research paper in 2020 that focused on 26 democracies between 1995 and 2018. We found that spending-based fiscal adjustments are notably more successful at lowering debt levels than tax-based adjustments, with successful adjustments being about two-thirds spending and one-third tax. We also found that spending-based adjustments tend to cause only small economic contractions, not significantly different from zero, while tax-based adjustments cause deep and long-lasting recessions.

A widely cited 2014 paper found that consolidations slow economic growth regardless of composition. That finding has shaped much of the subsequent policy debate. But the underlying narrative dataset has since been revised. In 2024, the International Monetary Fund released an updated version of the Alesina-style narrative consolidation dataset, extending coverage to 17 countries and revising shock magnitudes throughout the sample.

I use that updated data to revisit the composition question.

Growth effects

First, I examine the growth effects of fiscal consolidation. In line with prior literature, a one-percentage-point-of-GDP fiscal consolidation, regardless of composition, reduces GDP growth by about 0.4 percentage points in the year it occurs.

But once consolidations are separated into tax increases and spending cuts, the difference is clear.

A one-point-of-GDP tax increase reduces GDP growth by 0.59 percentage points in the year it happens. A spending cut of the same size reduces growth only by about 0.29 percentage points. In other words, the immediate growth cost of tax-based consolidation is roughly twice as large as the cost of spending-based consolidation.

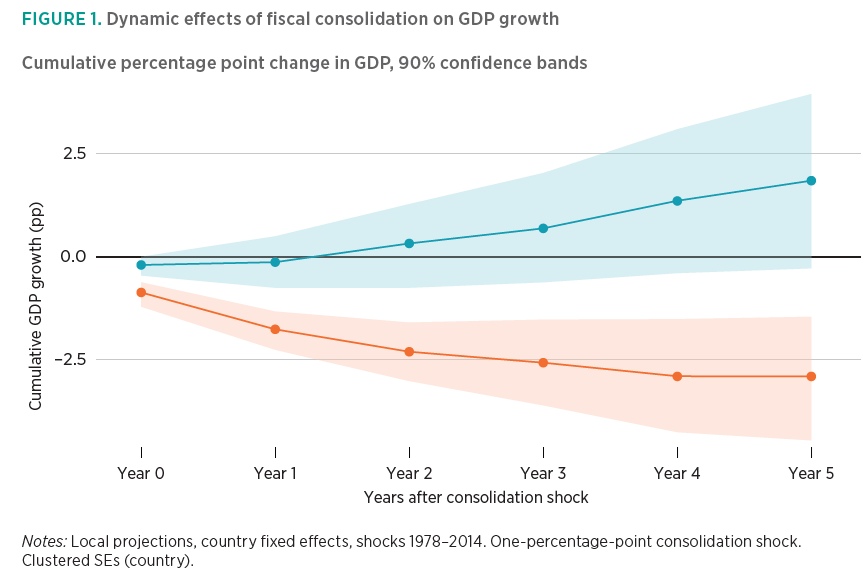

The gap widens over time, as figure 1 illustrates. Local projections out to five years show tax-based consolidations becoming increasingly costly: Cumulative growth losses reach nearly 3 percentage points after five years. Spending-based consolidations dip slightly at first, turn positive by year two, and reach a positive estimate of about 1.8 percentage points by year five.

By the fifth year, the two paths are nearly 5 percentage points apart.

Importantly, it is worth noting that most of the spending estimates are not statistically significant, with the year-five estimate only marginally significant at the 10% level. So, I cannot confidently claim that spending-based adjustments are expansionary. What I can say is that the tax estimates are consistently negative and highly statistically significant at the 1% level. Tax-based consolidations are contractionary, and increasingly so over time.

Debt reduction

Growth is one thing, but the ultimate goal of fiscal consolidation is debt reduction.

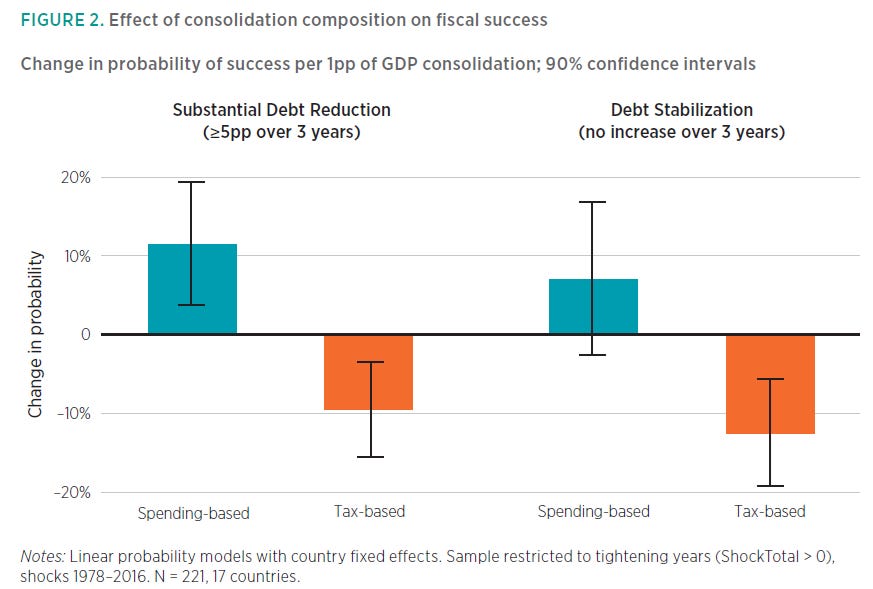

Using a strict definition of success (debt-to-GDP falling at least 5 percentage points within three years), a one-point spending cut raises the odds of success by 11.1 percentage points. A one-point tax increase lowers the odds by 9.5 points, as shown in figure 2.

Scale that result to a typical 2-point-of-GDP consolidation against a baseline success rate of roughly 24%: Spending cuts raise the predicted probability of success to about 46%. Tax increases reduce it to about 5%.

The tool politicians often reach for to look fiscally serious—higher taxes, especially on the rich—is often the one that makes actual debt reduction less likely.

The obvious follow-up question is whether this result holds only when debt is already high, where credibility concerns might dominate. I test that directly by interacting consolidation type with both high-debt and low-debt regimes. The interactions are small and statistically insignificant. In other words, I find no evidence that the spending-versus-tax result depends on the starting debt level.

Why might spending cuts work better?

The leading explanation is credibility. Spending reforms may be viewed as more durable than tax increases. A future legislature can undo a tax increase with a single vote, while rebuilding a program that has already been cut is often harder. Spending restraint may therefore send a stronger signal of fiscal discipline.

Spending cuts may also crowd in private investment by reducing expectations of future taxation and shrinking the government’s claim on resources. Tax increases, by contrast, can discourage work, saving and investment while doing less to convince markets that the underlying spending path has changed.

Not all spending cuts are equal. The broader literature generally finds that cuts to transfers and government consumption are more successful than cuts to public investment, which can undermine the growth needed to reduce the debt ratio.

But the basic lesson is clear: If the goal is actually reducing debt while doing the least damage to growth, the evidence points toward spending restraint, not tax increases.