The Real Social Security Debate: Who Should Bear the Adjustment?

The Fairest Way to Fix Social Security

The political theater around Social Security often obscures a fundamental question: When insolvency arrives, who bears the cost of adjustment? Do we choose deliberate reform or chaotic default, and do we choose to protect the most vulnerable or distribute pain equally across rich and poor alike? So far, policymakers have largely skirted these questions altogether.

The Accelerating Timeline

The Social Security Old-Age and Survivors Insurance (OASI) trust fund stands at $2.5 trillion today and is declining precipitously. Under current projections, complete depletion will happen in 2032—just six years away. What many don’t realize is that recent policy decisions have accelerated this timeline significantly.

In 2025, two pieces of legislation compounded the problem. In January, Biden’s Social Security Fairness Act expanded full benefits to 2.8 million public servants, bringing depletion forward by one year. Then in July, Trump’s “One Big Beautiful Bill Act” added a new deduction for seniors, effectively reducing taxes on Social Security benefits and advancing depletion by another six months. Combined, these politically popular moves shortened our runway by 18 months and added 0.28 percentage points to the payroll tax increase needed to close the 75-year funding gap.

Both parties, it seems, prefer expansion over sustainability when electoral politics are at stake.

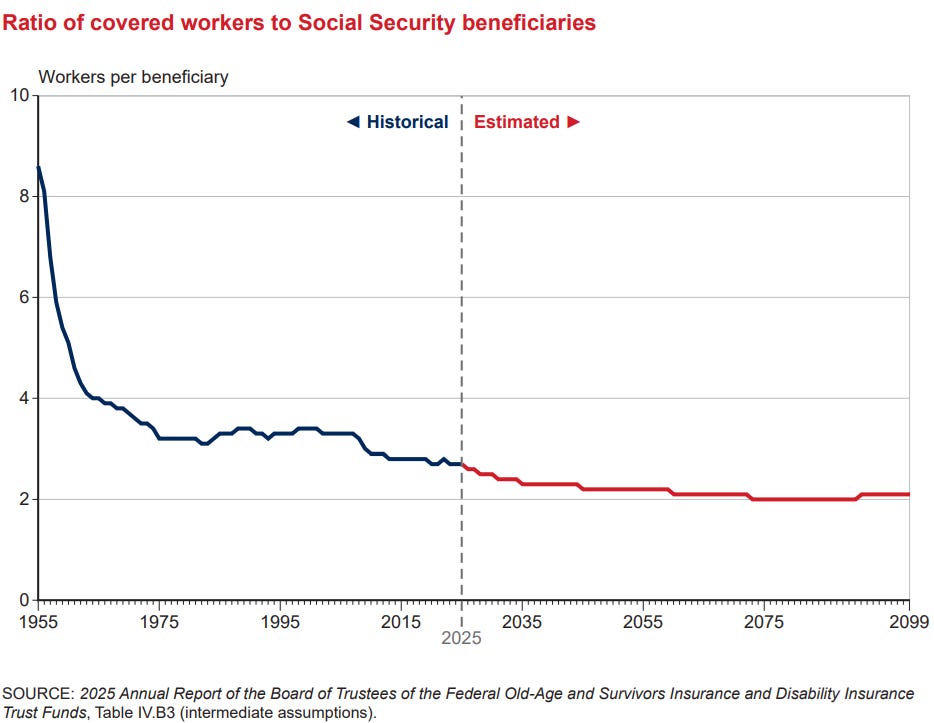

The Arithmetic of Demography

The fundamental challenge is straightforward: Social Security was designed for a different demographic reality. In 1955, nearly 9 workers supported every retired beneficiary. Today, that ratio has collapsed to 2.7 workers per beneficiary. By 2035, it will fall to 2.3 and continue declining thereafter, as shown in the figure below.

This is the predictable consequence of longer lifespans and lower birth rates, two trends that show no signs of reversing. The program was never designed to handle this kind of demographic inversion, and no amount of political rhetoric can change the underlying mathematics.

The program currently provides benefits to approximately 68 million Americans, including 54 million retired workers and their dependents. While many seniors remain dependent on these payments, the program has drifted far from its original intention of providing relief specifically for the poor elderly. Today, it functions more as universal old-age insurance, transferring resources from young workers, many struggling with student debt and stagnant wages, to retirees across the income spectrum.

The Coming Collision: $100 Trillion in Shortfalls

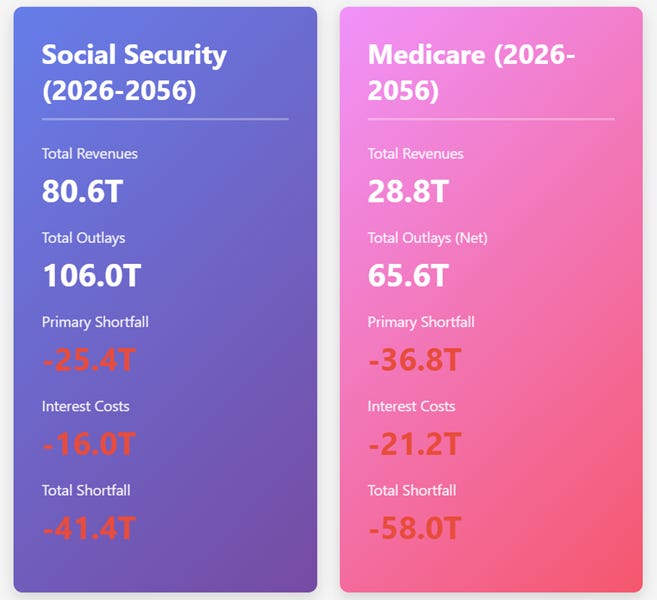

According to the latest Congressional Budget Office (CBO) 30-year projections, the fiscal picture is even grimmer than most realize. Social Security’s primary shortfall (outlays minus revenues) exceeds $25 trillion through 2056. This gap will generate an additional $16 trillion in interest costs as the government borrows to cover the difference, bringing Social Security’s total 30-year shortfall to more than $41 trillion.[1]

But Social Security doesn’t arrive at insolvency alone. As the illustration below shows, Medicare faces an even larger crisis, with a projected 30-year shortfall approaching $58 trillion when interest costs are included. Together, these programs face a combined shortfall near $100 trillion over the next three decades.

Let that sink in: one hundred trillion dollars. For context, that’s roughly three times current annual U.S. GDP.

Four Paths Forward

Policymakers face four options, though only one is economically sustainable:

Option 1: Across-the-Board Benefit Cuts

When the trust fund depletes, existing law requires an automatic 23% reduction in benefits. This reduction would hit every beneficiary equally, the poor widow receiving $1,919 monthly and the wealthy retiree collecting $4,152. While this approach is technically feasible, its cruelty is self-evident: Cutting benefits by 23% for someone living on $23,000 annually is categorically different from cutting benefits for someone receiving $50,000 annually.

Option 2: Raise Payroll Taxes

The alternative to benefit cuts is tax increases. To close the 75-year gap would require raising the combined FICA tax rate by roughly 4.3 percentage points, plus another 0.5 percentage points for Medicare’s Hospital Insurance shortfall.

But this approach doubles down on the program’s fundamental regressivity. Young workers, many already burdened with student loans and facing lower homeownership rates than previous generations, currently pay 7.65% in direct FICA taxes, with their employers paying another 7.65% (which economic incidence studies show ultimately comes from workers’ wages). Adding another 4.8 percentage points would push the total effective payroll rate on wages to nearly 20%, and that’s before income taxes.

This creates a perverse transfer: forcing low-income young workers, many earning $40,000 to $60,000 annually, to pay higher taxes to fund benefits for retirees across all income levels, including those with substantial retirement savings, assets and investment income.

Option 3: Borrow To Fund the Gap

Some suggest simply borrowing to cover the shortfall indefinitely. This is perhaps the most dangerous option. Markets are unlikely to tolerate nearly $100 trillion in additional public debt to fund insolvent entitlement programs. As my colleague Veronique de Rugy warns: “The moment Congress confirms such a path, expectations could shift instantly. Investors would recognize that the long-standing pattern of last-minute responsibility has broken down, that fiscal discipline is no longer forthcoming. That realization alone could trigger an immediate repricing of government debt.”

The result wouldn’t be gradual inflation over decades, but an immediate debt crisis as markets lose confidence in U.S. fiscal solvency. The economic devastation would dwarf any benefit cut.

Option 4: Structural Reform with Progressive Adjustments

The viable path combines structural reforms with progressive benefit adjustments that protect low-income seniors while requiring more from those with greater resources.

A Reform Agenda That Works

Six structural reforms could substantially narrow the funding gap:

Raise the retirement age to 68, then by three months annually until reaching 70. Index it to longevity thereafter. Life expectancy has increased dramatically since Social Security’s creation, but the retirement age has barely moved.

Change the Cost-of-Living Adjustment from CPI-W to chained CPI-U. The current formula overstates inflation for retirees by not accounting for substitution effects.

Extend the benefit calculation from 35 to 40 years of average earnings. This provision was set in 1977 and hasn’t been updated despite longer working careers.

Phase out nonworking spouse benefits for households in the top income quintile. These benefits were designed for an era of single-earner households, not dual-income professional couples.

Require Social Security Disability Insurance applicants to have worked 4 of the last 6 years, rather than 5 of 10. This change tightens disability eligibility while still protecting those with genuine work histories.

Include newly hired state and local government workers in Social Security. Closing coverage gaps ensures universal participation in the system.

The Means-Testing Question

But structural reforms alone won’t close the gap. The fairest additional adjustment is soft means testing, or put another way, limiting maximum benefits for high-income retirees.

Consider: The average monthly Social Security benefit in 2026 is $2,071, while some retirees collect the maximum $4,152. One approach would cap the maximum benefit at $3,000 monthly. This would preserve the social insurance character of the program while ensuring high earners receive less than the actuarially calculated maximum.

The choice is stark: Cut all benefits by 23%, hurting poor and rich alike, or scale back maximum benefits for high earners who have other retirement resources. The first path treats a widow surviving on $23,000 annually the same as a retiree with a $2 million 401(k) collecting nearly $50,000 in Social Security benefits. The second option recognizes that Social Security was meant to prevent poverty among elderly Americans, not maximize returns for the affluent.

The Window Is Closing

Six years remain before depletion. That’s barely enough time to implement gradual reforms that give workers and retirees time to adjust. Delay means harsher cuts, higher taxes, or market panic, none of which serve anyone’s interests.

The real Social Security debate isn’t about abstract ideological commitments. It’s about who bears the burden of adjustment: Should we protect vulnerable seniors, or should we distribute pain equally regardless of need? Should we burden young workers struggling with debt to fund benefits for affluent retirees? Or should we restore the program’s original purpose of preventing poverty among older Americans?

These are fundamentally moral questions. The only one remaining is whether we choose reform that reflects our values or default that reflects our cowardice.

The clock is counting down. In 2032, one way or another, Social Security will change. The only question is whether we control that change or whether we let demographics and insolvency control us.

[1] This calculation uses CBO’s projected effective interest rates calculated from their net interest and debt projections. This is the most accurate calculation method because it reflects the actual government borrowing costs, the mix of short-term and long-term debt, and changes in rates over the 30-year period (starting ~3.3% in 2026, rising to ~6.9% by 2056).

Thanks for laying this out so clearly! Are you and Veronique speaking to those in power about this?

The issue with cutting benefits is it breaks one of the fundamental benefits of the system -- you can rely on this income being there. People purchased homes with mortgages, moved into retirement communities etc etc based on the assumption that they get this many dollars a month.

And if you say fair enough, we won't cut the benefits of anyone who has already retired it makes the fairness problem you mentioned worse because young people are stil funding that money for the old but not getting it themselves.

And yes, it was a mistake to set it up this way but if I have to think: I always need to keep enough extra in investments to cover the possibility that the government decides to cut benefits again that's a problem.

Ultimately, I think a better move is to accept the tax increase while at the same time taking action to crater home prices. The wealthy old have huge home wealth but losing the value doesn't cost them their house and it gives young people a chance to own a house.

---

Well actually the right move is to just let in a bunch more immigrants, maybe even apply a higher tax rate to their income and use that to fix the shortfall but I might as well hope gold bars fall from the sky.