The Saez-Zucman California Billionaire Tax Proposal Ignores One Important Question

Emmanuel Saez and Gabriel Zucman have spent the better part of a decade arguing that billionaires are undertaxed. Their new NBER paper with Jasper Boll applies that thesis to California, documenting billionaire wealth growth, estimating effective tax rates as a fraction of wealth accumulation, and concluding that a 5% one-time levy could raise $100 billion with modest impacts on future income tax revenue.

Unfortunately, the paper entirely sidesteps the question it should be answering.

The California Billionaire Tax Act does not justify itself on abstract grounds of tax fairness. It justifies itself on a specific fiscal claim: that the One Big Beautiful Bill Act created a roughly $19 billion annual budget hole in California’s healthcare safety net that requires emergency revenue to fill. That is the premise on which the initiative was drafted, campaigned for, and is being sold to voters.

A new Hoover Institution analysis released this week by Joshua Rauh, Tom Church, Daniel Heil, Benjamin Jaros, and John Doran examines that premise in detail. What they find should be deeply uncomfortable for anyone relying on the Saez-Zucman framing.

The $19 Billion Figure Is a Fabrication of Averaging

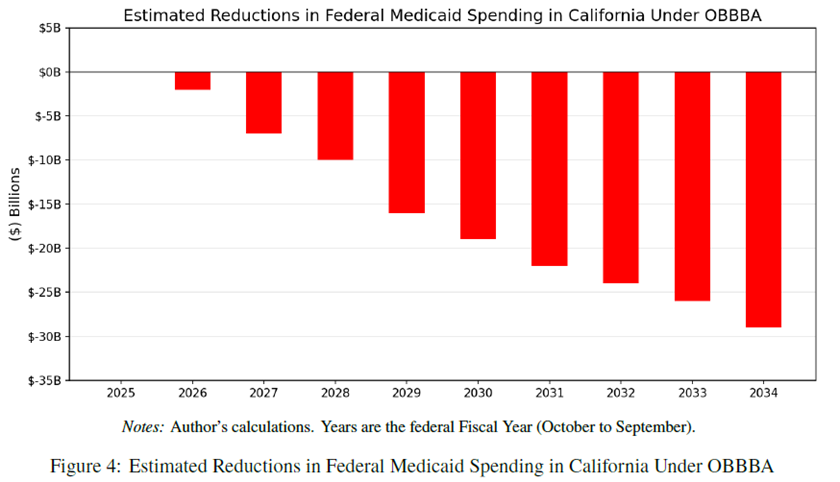

The proponents’ $19 billion annual shortfall figure is not an estimate of any actual annual loss. It is a cumulative ten-year federal Medicaid reduction divided by ten to produce a tidy annualized average. The Hoover paper exposes how misleading this framing is.

Using section-by-section CBO cost estimates, Rauh et al. find that the OBBBA will reduce federal Medi-Cal spending by $156 billion over ten years, a figure consistent with Kaiser Family Foundation estimates. But only 35% of those reductions occur through 2030. The annual reduction in 2026 is roughly $2 billion. It does not reach $19 billion in any single year until the early 2030s. Presenting a back-loaded worst-case scenario as an immediate annual emergency is not analysis; it is advocacy dressed up in decimal points.

Even the $156 billion headline does not translate into a $156 billion state budget problem. The Hoover paper carefully disaggregates who actually bears these reductions. The eligibility provisions, work, school, and volunteer requirements, account for $89 billion of the total. These provisions reduce Medi-Cal enrollment and therefore reduce both federal and state spending.

The state actually saves approximately $15 billion from these provisions over the budget window. The remaining $62 billion comes from limits on provider taxes and state-directed payments, which creates a funding gap that either the state backfills or providers absorb. The state is not automatically on the hook for the full $156 billion, and proponents who cite that figure as a “budget hole” are being deliberately imprecise.

The Tax Is Structurally Mismatched to the Obligation

Here is the deeper problem that the Saez-Zucman paper cannot paper over with wealth statistics: even if you accept the proponents’ revenue estimate of $100 billion at face value, the Billionaire Tax Act is the wrong instrument for this obligation.

The tax collects revenue over five years. Two-thirds of the OBBBA’s Medi-Cal reductions fall after 2030. The money runs out before the problem it supposedly addresses fully materializes. The Hoover paper estimates that after netting out lost income tax revenue from departing billionaires, the $40 billion in realistic collections is exhausted by 2029, the very moment the annual federal reductions start accelerating past $15 billion per year and growing.

California also has a $93 billion structural deficit projected through 2030, and a well-documented institutional habit of redirecting earmarked Medi-Cal funds toward general budget priorities. The Legislative Analyst’s Office (LAO) has noted this pattern explicitly with respect to excess MCO provider tax revenues.

Structural deficits are not new in California. The LAO notes that the legislature faced a $27 billion deficit in 2023-24, a $55 billion deficit in 2024-25, and a $15 billion deficit in 2025-26.

There is no mechanism in the Billionaire Tax Act that would prevent $100 billion in one-time wealth tax collections from disappearing into that deficit well before the largest federal reductions arrive. Saez and Zucman do not address this.

Medi-Cal’s Problem Is Spending Growth, Not Insufficient Revenue

The Boll-Saez-Zucman paper rests on the implicit assumption that California’s healthcare safety net is underfunded and that additional revenue would address the problem. The Hoover analysis demolishes this premise.

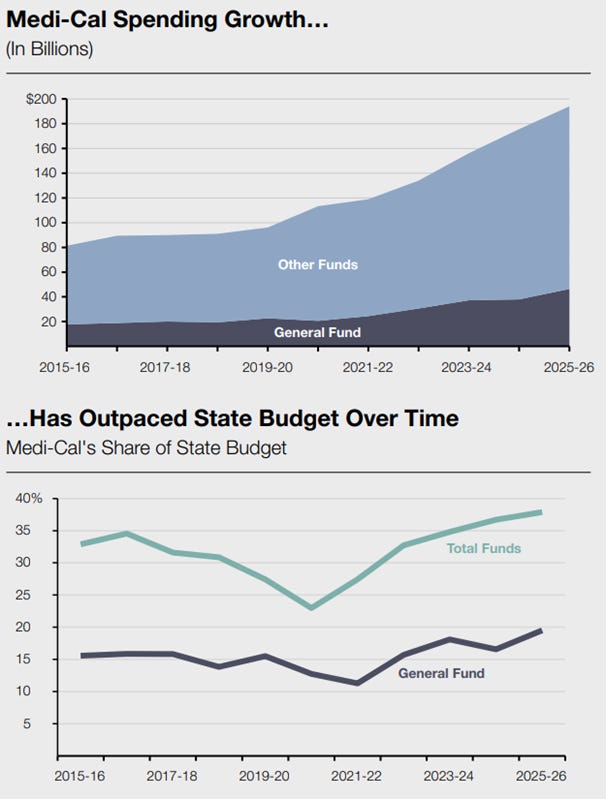

Medi-Cal expenditures have nearly tripled since 2011, growing from $54 billion to $185 billion annually. Over that same 15-year period, the Department of Health Care Services’ General Fund share grew at a compound annual rate of 9%, compared to 5.8% for all other General Fund spending. Medi-Cal is now the second-largest General Fund program in the state, comprising 40% of spending. If its General Fund share had simply been held at the post-ACA, pre-COVID average of 15.7%, the state would save roughly $9.8 billion per year, nearly $88 billion over ten years.

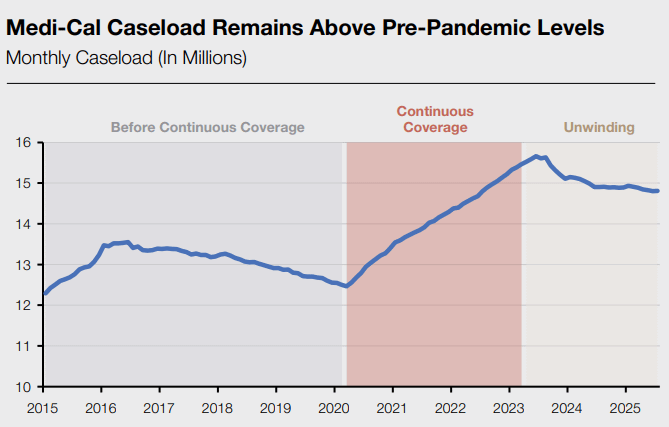

The explosion in Medi-Cal spending is the result of changes in the law that have massively increased the population covered by the program. There were around 12 million on Medi-Cal in 2015, and about 15 million today, or nearly 4-in-10 Californians. The LAO also suggests that per-enrollee spending can be explained by major policy changes enacted since 2017-18, such as the expansions of comprehensive coverage to undocumented adults.

And what did California get for this extraordinary spending growth? Quality of care has remained below the national median across virtually every measured dimension for both adults and children, consistently and without interruption. The Hoover paper documents this through five rounds of Consumer Assessment of Healthcare Providers and Systems survey data. In 2024, Medi-Cal ranked below the 50th national percentile on all eight quality metrics for both adults and children. The program’s challenges are structural, not fiscal. Pouring more money into a poorly designed system does not fix the design.

California Has the Tools. It Chooses Not to Use Them.

Perhaps the most important finding in the Hoover paper is that California does not actually need new revenue to address the gap that would remain after accepting OBBBA’s eligibility defaults. If the state accepts the federal work and community engagement requirements, which represent the default condition of federal law, not some radical policy imposition, the remaining federal reductions the state would need to address fall to approximately $67 billion over ten years.

The Hoover analysis identifies policy levers already within the state’s control that generate over $125 billion in ten-year savings without any new revenue source: reversing discretionary Medi-Cal coverage expansions for undocumented immigrants ($37 billion over ten years) and returning the program’s General Fund share to its post-ACA, pre-COVID average ($88 billion over ten years). That is nearly double the remaining obligation.

None of this requires taxing anyone. It requires California to make different spending choices than it has made over the past decade. The Saez-Zucman paper does not engage with this alternative because doing so would require acknowledging that the “fiscal emergency” framing is, at minimum, incomplete.

The Real Problem with the Proposal

Boll, Saez, and Zucman have written a paper about billionaire wealth. It is not, despite appearances, a paper about whether the California Billionaire Tax Act makes fiscal sense. None of it is relevant to whether a one-time residency-triggered levy is a structurally sound way to address a back-loaded, partially discretionary reduction in federal Medicaid cost-sharing.

One of the paper’s authors helped design the ballot initiative. The paper’s framing reflects that involvement. When you begin with the conclusion that billionaires should pay more and work backward to the policy, you tend to produce analysis that answers the question you want to answer rather than the one the voters will actually be deciding.

The Hoover Institution paper asks the right question. Its answer is that the fiscal premise of the Billionaire Tax Act fails on its own terms, in magnitude, in timing, and in structure. That finding will not make it into the New York Times op-ed. But it should inform how Californians vote in November.

Hoover has always been a far, far right-wing ideological think tank funded by multi-billionaires needing an respectability organ to lobby politicians and find "expert" testimony in court and to Congress the self interests of their donors. For the past half century, most think tanks have similar sponsors to cranking out tons of cookie-cutter public policy papers (replacing academic economists ensuring lifelong tenure by avoiding policy) -- Gov't, even if well-intentioned, will screw up or worse will expand their size, monopolies are temporary or caused by gov't itself, incentives for the poor must be all stick but for the rich or business must be all carrots, externalities and asymmetric information can be reconciled by market actors eventually via the Coase Thm (I saw Coase speak on a panel of 5 Chicago Nobel Prize winners), likewise, gov't intervention blamed for all macro problems (inflation, recession, stagnation, inequities, supply shortages, trade imbalance, devaluation), and free markets, targeted vouchers, transferable ownership rights will work in the very long run (unless downturns, stagnations, interest on the debt, or the resultant kleptocracy (like Russia's and China's) spoil the party by extorting all wealth like Putin did.