Washington’s Millionaires Tax Unlikely to Raise Projected Revenues: Lessons from California

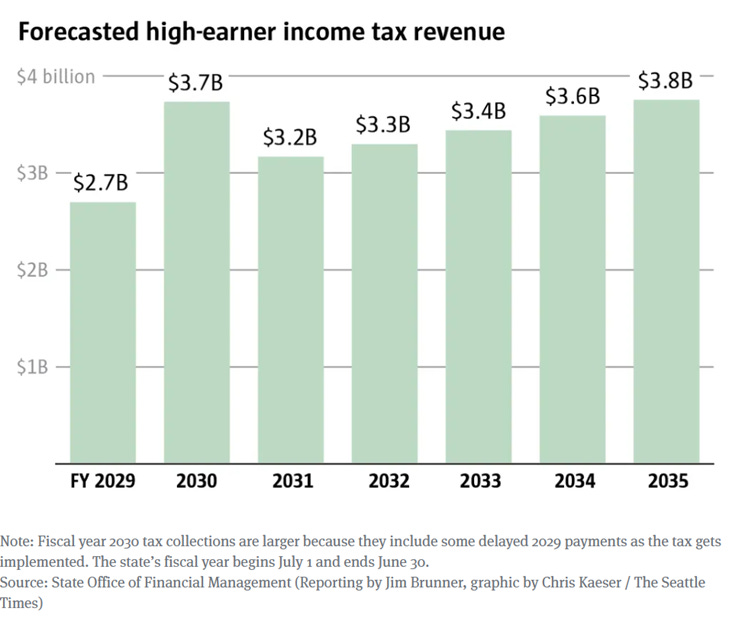

Washington Gov. Bob Ferguson this week signed into law a new 9.9% tax on income above $1 million, marking a historic shift for a state that has long gone without an income tax. Supporters have framed the policy as a step toward a fairer tax system, with revenues projected to raise $3–4 billion annually to fund education, healthcare and other public services, as shown in the Seattle Times figure below.

The size of the tax increase is substantial. Once fully implemented, Washington’s combined state and local top marginal rate will exceed 18%. When combined with federal taxes, top earners will face marginal rates approaching 58%.

But the policy faces immediate legal and political uncertainty. For more than 90 years, the Washington Supreme Court has held that income constitutes property under the state constitution, meaning it must be taxed uniformly rather than at graduated rates. On that basis, former Attorney General Rob McKenna and the Citizen Action Defense Fund have already filed suit challenging the tax’s constitutionality. At the same time, opponents are pursuing a referendum to put repeal directly before voters.

Notably, the tax will not take effect until January 1, 2028, with the first payments due in April 2029. That delay gives high-income taxpayers years to adjust their behavior in advance, whether by shifting income, changing residency or restructuring how and when they realize earnings. As the chart below demonstrates, nearly 15,000 high-income individuals already left the state in the three years following the enactment of a capital gains tax. Static projections that ignore these responses are therefore especially unreliable.

Even setting all those challenges aside, there is a further reason for skepticism of the millionaires tax: The revenue projections themselves are almost certainly too optimistic.

One empirical guide we have comes from California’s Proposition 30. In a careful 2024 study using administrative tax data, Joshua Rauh et al. find that a relatively modest 3-percentage-point increase in top marginal rates, adopted in 2012, led to large behavioral responses among high earners. These responses—primarily changes in reported income rather than migration—eroded 45% of the proposition’s expected revenue within the first year and over 60% within two years.

At first glance, Washington’s policy might seem comparable. But on the economically relevant margin, its effects will be much larger.

What matters for behavior is not the statutory rate increase itself, but the change in the net-of-tax rate—the share of an additional dollar of income that taxpayers keep. On this margin, Washington’s new tax represents a shock roughly 2.8 times larger than California’s Proposition 30.

If a smaller tax increase in California wiped out more than half of projected revenues within two years, a tax increase nearly three times as large risks eroding an even greater share of the tax base. A simple extrapolation suggests that the Evergreen State could lose more than 100% of projected revenue. But that is precisely the point: The behavioral response implied by the evidence is large enough that it could nearly eliminate the expected revenue altogether.

The static estimates of revenues in the $3–4 billion range overlook a much broader problem. When high earners leave, the state does not just lose their income tax revenue. It also loses the sales taxes they pay, the property taxes they contribute and the business and occupation taxes tied to the firms they own and operate. Many of these individuals are also major employers and investors, supporting thousands of jobs and significant local economic activity. As their spending, investment and business activity shift elsewhere, the erosion of the tax base extends well beyond the income tax itself.

There is one important nuance worth acknowledging. California already had a high state income tax prior to Proposition 30, whereas Washington is introducing this tax from a base of zero. That difference could cut in either direction. On one hand, the introduction of a new, high marginal rate may represent a larger behavioral shock. On the other hand, California’s taxpayers may already have had more established mechanisms for income shifting and tax planning. Even so, the core lesson from the evidence remains: High-income taxpayers are highly responsive to marginal tax rates.

The broader takeaway is straightforward. Ignoring behavioral responses leads to systematically inflated revenue forecasts, particularly when targeting a small, highly mobile group of top earners. If this “Millionaires Tax” holds up to legal challenges, Washington is about to test that lesson in real time.

I was born and raised in Washington, left for work, and have been back for a bit over six years. The amount the state extracts in taxes (often hidden in the form of higher costs for goods and services) has gone up significantly but not enough to keep up with increases in spending. But the quality and quantity of tangible benefits from that spending is decreasing. We’re told it’s “more for more” but it’s really “less for more.” None of the people pushing for the spending consider the efficacy of that spending.

One of many schemes I have come up with is that every bill has to list all expected consequences -- not intended, but expected, to get both the good and bad listed. If a law produced other consequences, citizens could sue to void it as defective and throw legislators out of office. It was partly to catch rosy predictions like this (another impetus was laws named after victims which would have had no effect on the crime they were inspired by). I later decided it was unnecessary, since both were fraud, and citizens can always sue politicians for that in my Chartertopia.