What History Tells Us About Tariffs and Why It Matters Now

Last month, the Supreme Court handed down one of its most consequential trade decisions in decades. By a 6-3 vote, the court ruled that President Trump’s use of the International Emergency Economic Powers Act (IEEPA) to impose sweeping tariffs, including the “Liberation Day” reciprocal tariffs and duties on Canada, Mexico and China, was unlawful. Chief Justice Roberts was blunt: IEEPA “contains no reference to tariffs or duties,” and the two words the administration leaned on cannot “bear such weight.”

Hours after the ruling, Trump signed a proclamation imposing a new 10% global surcharge under a different statute (later raising this to the 15% maximum allowed), signaling that the era of aggressive tariff policy is far from over.

Into this moment comes a new working paper from two Northwestern University economists, Tamar den Besten and Diego Känzig, which presents a comprehensive empirical study of American tariff policy over nearly two centuries. Published by the National Bureau of Economic Research in February 2026, the paper draws on nearly 200 years of U.S. data from 1840 to 2024 to ask a deceptively simple question: What actually happens to the economy when tariffs go up?

The Challenge of Learning from History

Studying tariffs is harder than it sounds. The obvious approach of comparing economic performance before and after a tariff change runs into a fundamental problem: Governments rarely raise tariffs at random. They tend to increase tariffs when they’re running budget deficits, trying to protect struggling industries or responding to recessions. A naive look at the data conflates the effects of the tariff with the economic conditions that caused it in the first place.

Den Besten and Känzig tackle this problem with a “narrative” approach borrowed from macroeconomic research on monetary and fiscal policy. They read through congressional records, presidential speeches, historical accounts and the United States Statutes at Large, cataloguing 35 major tariff events going back to 1840. For each one, they ask: Was this tariff driven by ideology or political dealmaking, protectionism for its own sake or free-trade conviction? Or was the tariff a response to economic stress, such as wartime revenue needs or a recession? Only the former category, which the authors call “plausibly exogenous,” is suitable for identifying the true causal effect of tariffs on the economy.

Twenty-one of the 35 events made the cut. The exogenous list includes the McKinley Tariff of 1890 (driven by Republican protectionist ideology), the Underwood-Simmons Tariff of 1913 (a Democratic free-trade reform), Smoot-Hawley (motivated by distributional politics, introduced before the 1929 crash), successive General Agreement on Tariffs and Trade liberalization rounds and both rounds of the 2018-19 Trump tariffs. The endogenous list includes the Civil War revenue acts and the 1921 Emergency Tariff, which was enacted explicitly to rescue distressed farmers during a sharp postwar recession.

What the Data Show

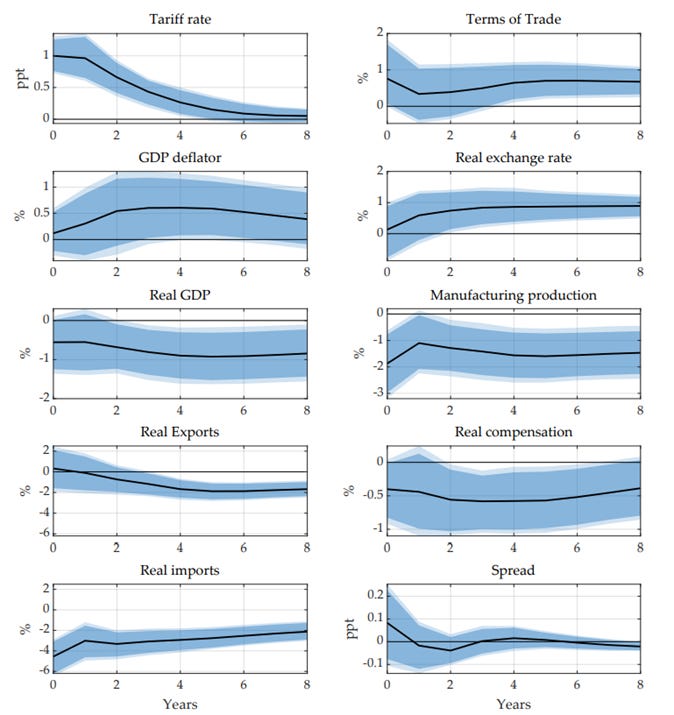

Using these 21 exogenous tariff events as a statistical instrument (a way of isolating genuine policy-driven variation from noise), den Besten and Känzig estimate how the U.S. economy responds to a tariff shock. Their benchmark is a one-percentage-point increase in the average tariff rate on dutiable imports.

In the authors’ model, the first economic response to tariffs is that imports fall sharply, about 4% on impact, which is precisely what tariffs are designed to do. But the story doesn’t stop there. Exports, after a brief pause, also decline, falling roughly 2% at their trough. The exchange rate appreciates as import demand contracts, which erodes the competitiveness of American goods abroad. Trading partners also retaliate and adjust their own sourcing. The result is a broad contraction in trade on both sides of the ledger, as shown in the authors’ figure below.

Most striking is what happens to domestic production. A one-percentage-point tariff increase leads to a peak decline in real GDP of around 0.9%, a large and persistent effect that continues for at least 8 years after the shock. Manufacturing output, the sector tariffs are most often designed to protect, falls by more than 1.5% at its peak. Real wages for manufacturing workers also decline.

In other words, tariffs do not succeed in their stated goal of shielding American industry. The general-equilibrium effects—higher input costs, a stronger dollar, weaker exports, reduced foreign demand—more than offset whatever protection individual sectors might receive.

This may also largely explain why employment in the manufacturing sector was more than 100,000 jobs below pre-election trends by the end of 2025. The chart below shows changes in manufacturing employment in relation to the pre-election (Nov 2022-Nov 2024) trend.

Tariffs also raise prices: The GDP deflator increases by about half a percentage point after two years and stays elevated about 6 years after the shock before subsiding. The inflationary punch of tariffs, the authors find, is real but largely self-limiting, dampened by the very economic weakness tariffs create.

Why the Method Matters

The authors of this study show what happens if you ignore the endogeneity problem. When they use their list of tariff changes driven by economic conditions (the endogenous events) as if they were exogenous, the results look completely different. Imports and exports show little response, output doesn’t clearly decline, and prices fall rather than rise. The reason is that these tariff changes were themselves reactions to economic downturns, so the data are picking up the recession, not the tariff.

A recursive VAR approach, the standard econometric workaround that simply assumes tariffs are exogenous, produces similarly misleading results. In that specification, the GDP deflator falls sharply, a pattern that shows up in other recent historical studies of tariffs. Den Besten and Känzig argue that this is an artifact of misidentification, not a genuine finding.

Modern Tariffs May Be Worse

One of the paper’s more nuanced findings concerns how tariff effects have changed over time. In the pre-World War II era, when the United States was on the gold standard, tariff increases caused inflation and a gradual erosion of export competitiveness through the classic price-specie-flow mechanism: The trade surplus from lower imports attracted gold, expanded the money supply and pushed up prices, which eventually hurt exports.

In the postwar period, the transmission is different and, in some ways, more painful. With floating exchange rates, the dollar appreciates immediately following a tariff shock, directly hammering exports without the cushion of a gradual adjustment. Trading partners, operating in a world of reciprocal trade agreements, retaliate more quickly.

The result is that modern tariff shocks work more forcefully through demand destruction: Exports fall fast, output contracts sharply, and prices may actually decline because the demand collapse overwhelms the cost-push pressure. The stagflationary combination of rising prices and falling output that characterized older tariff regimes gives way, in the modern era, to something closer to a deflationary contraction.

What This Means Now

The Supreme Court’s IEEPA ruling struck down tariffs that raised effective tariff rates from about 2.5% to more than 13%, their highest level since the early 1930s.[1] Trump immediately responded by invoking Section 122 of the Trade Act of 1974, imposing a fresh 10% (later 15%) global surcharge that must be renewed by Congress within 150 days. Section 232 tariffs on steel, aluminum and autos remain in place. The tariff era is not over; it has shifted legal grounds.

Den Besten and Känzig’s findings are directly relevant to this moment. Their paper suggests that the economic damage from tariffs does not come mainly from the direct cost of higher import prices, but from the cascade of second-order effects: the stronger dollar, the retaliatory response, the contraction in exports and the broader slowdown in economic activity. Their estimates imply that even a one-percentage-point increase in the tariff rate eventually costs the economy nearly one percent of GDP. The tariff increases of the past year were magnitudes greater than this.

The paper also offers a subtle warning about interpreting recent data. During the IEEPA tariff period, prices rose and output slowed, a pattern consistent with the historical stagflationary effects den Besten and Känzig document. But as tariffs come down, the authors’ model suggests the reverse: Lower trade barriers support trade volumes, boost output and relieve cost pressures. How much relief the economy gets will depend heavily on how aggressively the administration pursues replacement tariffs under other authorities and how quickly trading partners respond.

Nearly two centuries of American history, carefully read, tell a consistent story. Tariffs may feel like protection. But the data suggest they function more like a tax, one whose costs are borne most heavily by the economy they were meant to defend.

[1] Author’s calculation using imports and customs duties data.

I'm alsway a little skeptical about empirical results that confirm my opinions too perfectly :), but this looks pretty solid.