Criticisms of the One Big Beautiful Bill: From Reasonable to Ridiculous

Several claims are being made about the recently enacted One Big Beautiful Bill Act (OBBBA), many of which are exaggerated, misleading or outright indefensible. A recent letter published by the Congressional Budget Office (CBO) has been touted as proof of OBBBA’s negative effects, notably in a fact sheet by House Budget Democrats. But while some of the fact sheet’s claims have merit, others are less legitimate, as a closer look at the facts shows.

Claim #1: It “adds over $4 trillion to the national debt.”

The CBO’s official cost estimate of OBBBA found that the bill would increase deficits by $3.4 trillion relative to current law, resulting from $4.5 trillion in revenue loss minus $1.1 trillion in spending reductions.

This understates OBBBA’s effect on the deficit, though. Once debt service costs are factored in, the deficit increase jumps to $4.1 trillion. Moreover, extension of the act’s temporary provisions—such as no tax on tips, overtime or auto loan interest—would push this interest-inclusive cost up from $4.1 trillion to $5.0 trillion.

Republicans have repeatedly countered that OBBBA will pay for itself through a combination of faster growth, proposed discretionary cuts and higher tariffs. These claims have been excellently addressed by Veronique de Rugy, so I won’t belabor them.

But I will highlight two Republican inconsistencies: First, if you’re claiming faster economic growth from OBBBA’s tax cuts, then you should also account for slower economic growth from Trump’s tariff-tax hikes; and second, the president’s budget proposal is just that—a proposal. Until those savings are signed into law, no one should be using them to justify deficit increases

This claim is accurate.

Claim #2: It “leaves working families worse off.”

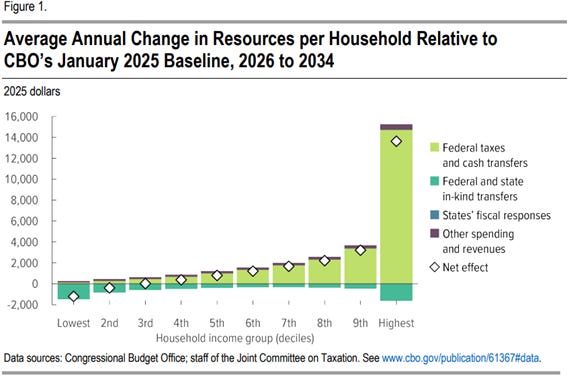

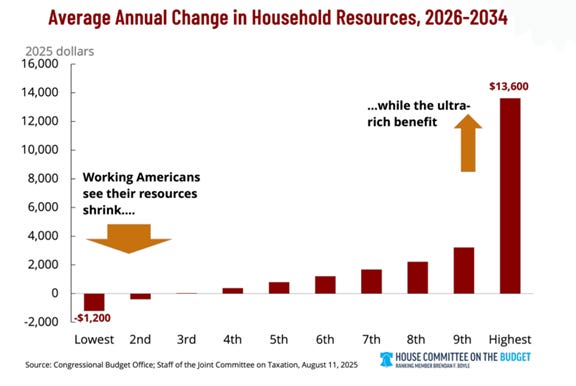

Compare the two charts below. The first comes from CBO’s letter, while the second comes from the House Budget Democrats’ fact sheet.

CBO’s chart breaks down the estimated total change in resources by income across four categories (depicted by different colors), whereas the House Budget Democrats’ chart illustrates only the net effect (represented by the diamonds in CBO’s chart). The two major components in CBO’s chart are federal taxes and cash transfers (light green) and federal and state in-kind transfers (blue-green).

It’s difficult to tell from CBO’s chart, but the data underlying CBO’s figures confirm that every income decile in its analysis received both a tax cut (or increased cash transfer) and a reduction in government transfers.

There are two obvious responses someone might have to this. The first is, “But look at how large the tax cut is for the richest 10%—it dwarfs everyone else’s tax cut, especially the poorest. Unfair!” I’ll address this later under claim #3.

The second likely response, which I think is much more interesting, has to do with the net effect that the fact sheet highlighted: “The poorest 10% lose $1,200 in resources. See, the poor are worse off!”

There are a few problems with this conclusion. First, it makes no distinction between who is losing benefits or why. It doesn’t mention removing illegal immigrants from Medicaid, strengthening work requirements for food stamps, or implementing policies aimed at reducing improper payments, as scholars at the Economic Policy Innovation Center (EPIC) have pointed out.

Those reforms seem like common sense. Why would you want welfare benefits to go to people who don’t qualify, who voluntarily choose not to work or who are here illegally? Surely taxpayers deserve a more nuanced discussion of welfare policies rather than simply lumping all welfare into one bucket.

Second, this response implies that the only relevant detail is how much people receive from welfare programs. Consequently, the negative effects of welfare, such as lost independence and reduced motivation, are entirely ignored.

Milton Friedman famously highlighted these effects 45 years ago in his “Free to Choose” series:

In one interview he spoke with a hospital orderly named Richard Brown who earned too much to qualify for Medicaid for his daughter’s healthcare needs. To qualify, he would have needed to cut back his hours or quit his job entirely—the opposite outcome you’d hope for from welfare.

Certainly, welfare programs have changed since that video was produced; but on the margin, people still face the decision between earning more or preserving their welfare benefits. Perhaps even more concerning was this insight from Brown’s wife:

I think a lot of people are capable of working and are willing to work, but it's just the way it is set up. It, the mother and the children are better off if the husband isn't working or if the husband isn't there. And this breaks up so many poor families.

Brown was able to resist the temptation to work less, but not everyone can. Take the case of the Ramsay family in England. The father, Steven Ramsay, had voluntarily gone seven years without a job because his family was receiving as much from England’s welfare program, known there as “Social Security,” as he could have earned from a job. Ramsay’s wife, Maureen, said this about their situation:

My opinion, anyway you feel as they own you. You know, there is no other way of putting it. Say I got a job tomorrow, because I needed something, well I know that means I've got to go down there and report it. Because I couldn't go into the job because you'd be looking over your shoulder thinking well the Social Security is coming in. And I'm going to be done for it. It's just hopeless, you can't fight against that.

So, while it’s true that some government resources won’t be available under OBBBA, that’s not the same as saying people will be worse off without those resources. In fact, I would venture to say that there are many people who would be better off if the government stopped paying them to remain poor. Of course, there are people on welfare who are truly in need; however, instead of treating welfare like it’s the cure for poverty, we should have an honest discussion about its effects and consider whether there are other solutions besides a government handout.

This claim is exaggerated.

Claim #3: It “gives the ultra-rich a massive tax cut” while “working-class people get no tax cut.”

This complaint by House Budget Democrats comes from a Joint Committee on Taxation (JCT) analysis of OBBBA. Specifically, the analysis found that taxes on households earning under $15,000 will increase by more than 9% while those making over $1 million will get a tax cut of $97,000. Unfair!

Well, maybe not.

The table below converts JCT’s estimate into the average tax per taxpayer before and after OBBBA. The 9% tax increase for those with income under $15,000 equates to just $25, slightly bumping up the average tax rate for those taxpayers to 4.4%. By contrast, those with income over $1 million will still pay an average of more than $857,000 in taxes even after the $97,000 tax cut, leading to a post-OBBBA tax rate of 27.8%.

So yes, a 9% tax increase on the poorest Americans sounds like a lot, but it loses its teeth when you realize it’s $25. Add that to the fact they’re paying a tax rate less than one-sixth what the highest earners pay and that every other income group received a tax cut of 10% or more, and this claim becomes near-meaningless.

The House Budget Democrats’ selective use of JCT’s analysis rather than the CBO letter is also noteworthy. CBO’s letter relies upon the same JCT data but notably uses income deciles rather than income level. Thus, as mentioned earlier, the CBO letter shows that every income decile received a tax cut, with the bottom 10% receiving a tax cut of $119 and the top 10% getting a $14,708 tax cut. This doesn’t align well with claim #3.

At the very least, claim #3 is misleading.

Claim #4: It “sets a new precedent for wealth transfers to the ultra-rich.”

Or, as the title in the House Budget Democrats’ fact sheet states, OBBBA “steals from the poor to give to the ultra-rich.”

The government does indeed conduct wealth transfers from the poor to the rich. One instance is the U.S. sugar program, which props up prices for sugar producers at the expense of American consumers. But the suggestion here is that cutting taxes and reducing welfare is a wealth transfer. It’s not.

That’s because wealth transfers occur when the government takes what is created by one person and gives it to someone else. OBBBA does do that, but not in the way House Budget Democrats have described. In fact, it limits the scheme of taking from those who produce today and giving to those who don’t; it doesn’t reverse the direction as suggested.

The real transfer scheme that OBBBA exacerbates is alluded to but otherwise neglected: the intergenerational transfer from future taxpayers to today’s. By financing tax cuts with new debt, we are forcing future generations to pay for more of today’s government.

That doesn’t mean all deficit-financed tax cuts are wrong. Tax cuts that truly lead to faster economic growth—such as business expensing, which was included in OBBBA—can be justified on the grounds that they will lead to higher future incomes. The problem is that those pro-growth tax cuts make up only a small portion of OBBBA’s deficit increase, making most of OBBBA a wealth transfer to today’s voters without a commensurate benefit to future taxpayers.

Claim #4 completely misses the mark on what constitutes a wealth transfer and omits the genuine source of transfers that will result from OBBBA, making this claim indefensible.